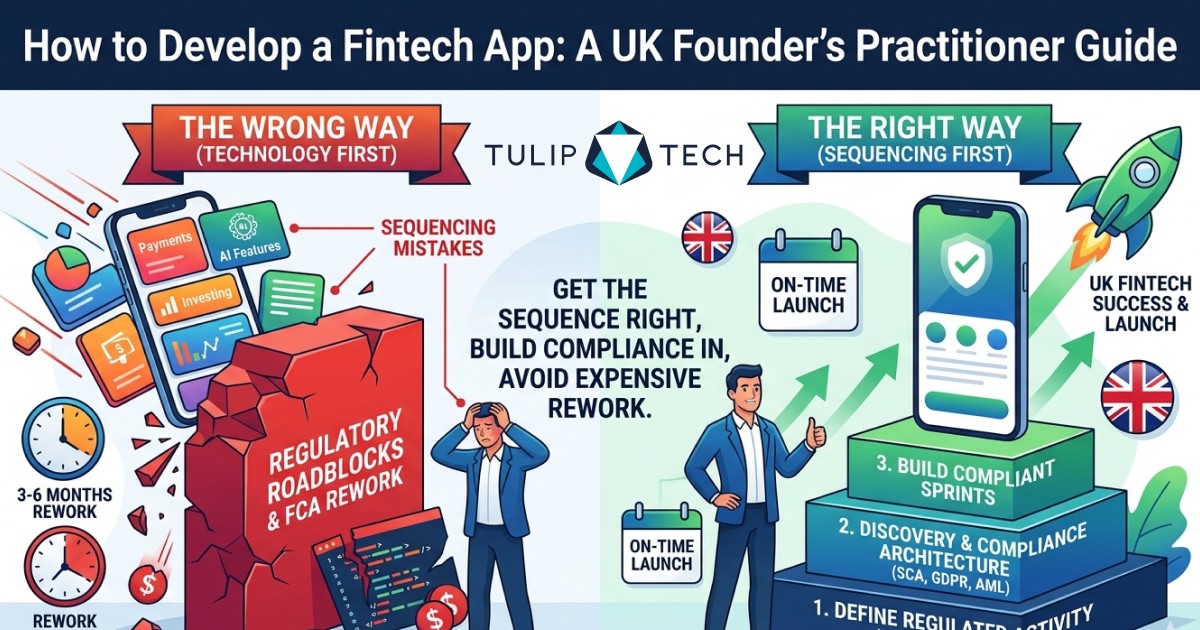

Almost every guide to building a fintech app opens with the tech stack and a feature list. For a UK build, that is the wrong place to start, and the founders who start there pay for it later.

The expensive mistakes in UK fintech are not coding mistakes. They are sequencing mistakes: building before the regulated activity is defined, treating compliance as a final phase, or assuming any capable app team can ship a regulated product.

This guide takes the opposite approach. It names the five misconceptions that cost most UK founders three to six months of rework, corrects each one, and then walks the right sequence end to end, from FCA permission through to post-launch compliance.

The misconception that sets the wrong order

The first and most expensive myth is that a fintech build starts with the technology. It does not. It starts with a single question: which regulated activity does this product perform?

The answer decides everything downstream. A payment institution, an electronic money institution, a credit broker, an account or payment information service provider under PSD2, and an exempt support tool each carry different FCA permissions, and each permission changes the architecture, the timeline, and the cost. This guide is the build companion to our pillar on the top fintech app development companies, which covers choosing the partner; here the focus is the process itself.

Get the regulated activity wrong and you build the wrong product confidently. Get it right and every later decision, from data residency to authentication, has a clear reference point.

Myth one: you can choose the tech stack first

Founders love this question because it feels concrete. The honest answer is that the stack is downstream of the regulated activity and the compliance architecture, not the starting point.

That said, the stack does carry real cost and capability differences once the activity is set. React Native and Flutter both ship compliant fintech UIs, with React Native offering the deeper UK hiring pool and Flutter offering tighter visual control. On the backend, an event-driven design built on Node.js or Go handles the webhooks and idempotency that payment flows demand better than a naive request-response model.

Library choices matter too: FIDO2 and passkey libraries for Strong Customer Authentication, a velocity-counter store such as Redis for fraud signals, and a fraud-model runtime for on-device or low-latency inference. Choose the stack to serve the regulated activity, not to chase novelty, and the build stays maintainable.

Myth two: compliance is a phase you do at the end

The second myth treats FCA, PSD2, and GDPR as a checklist applied after the build. Every one of those decisions lives in the architecture, and by the time you reach testing they are set and expensive to undo.

Strong Customer Authentication is not a screen; it is a flow whose authentication data must be dynamically linked to the payment amount and payee. UK GDPR data residency is a deployment decision made before the first environment is provisioned. PCI DSS scope is a network-segmentation decision: a product handling 6 million-plus card transactions a year sits at Level 1 and needs a Qualified Security Assessor audit, while one under 20,000 e-commerce transactions sits at Level 4 with a far lighter burden, and that threshold changes the whole architecture.

Build the compliance architecture in discovery. A partner who proposes to "handle compliance during testing" is telling you they have not done this before.

Myth three: any good app team can build fintech

A team that ships excellent consumer apps can still sink a fintech build, because the failure modes are regulatory, not technical. The code can be clean while the product cannot launch.

Regulated delivery experience shows up in the certifications a partner holds and expects: ISO 27001 as a baseline, Cyber Essentials Plus for UK practice, SOC 2 Type II for any B2B or enterprise fintech buyer, and PCI DSS attestation for card handling. It also shows up in the reference architecture they arrive with, covering a banking core, an Open Banking aggregator, an identity provider, and a fraud layer.

A generalist builds those from scratch on your time and budget. A specialist arrives with them, which is the difference between a build that absorbs the regulatory load and one that discovers it at month four.

Myth four: Open Banking is just an API integration

The fourth myth reduces Open Banking to plugging in an API. In reality it is a regulatory build decision that shapes your cost, timeline, and FCA burden.

You either become a regulated third-party provider yourself, an account information service provider or payment initiation service provider, or you integrate a licensed aggregator such as TrueLayer, Yapily, or Plaid. Becoming a TPP gives control and removes per-transaction fees at the cost of your own FCA authorisation and ongoing compliance. Integrating an aggregator is faster and shifts the regulatory burden, at the cost of a dependency and usage fees.

Either path carries UK-specific plumbing: AISP versus PISP scopes, the 90-day re-authentication requirement that forces a consent-renewal flow, FCA-registered TPP status, and the sandbox-to-production certification path under the UK Open Banking Standard. None of that is "just an API".

Myth five: the MVP can skip security and AML to launch faster

The final myth treats security, AML, and KYC as features to add after launch. For a regulated product they are launch-blockers, not enhancements.

A fintech MVP still needs identity verification, sanctions and PEP screening, transaction monitoring, and an audit trail, because without them the product cannot legally operate. The right move is to scope the smallest version that performs the regulated activity safely, not the smallest version that looks like a finished app.

What an MVP can defer is breadth, not compliance. Cut the third account type, the loyalty programme, and the analytics dashboard; never cut the SCA flow, the KYC gate, or the safeguarding of customer money.

The right sequence, step by step

With the myths cleared, the build follows a defined sequence where each step produces an output the next one depends on.

Step one: define the regulated activity and target permission

Name the FCA permission the product needs before anything else, because it sets the safeguarding, capital, data, and authentication requirements. Write it down and brief every partner against it, not against a generic "compliant app".

Step two: discovery and compliance architecture

A UK fintech discovery runs £8,000 to £15,000 over three to five weeks and maps the FCA pathway, the PSD2 SCA flow, the GDPR data flows, the KYC and AML integration, and the PCI scope. The output is an architecture that has the compliance decisions designed in, plus a risk log and a written specification every developer can quote against.

Step three: design and prototyping

Design the regulated journeys first: onboarding with identity verification, the SCA challenge, and consent capture. These are the screens that fail user testing and regulatory review, so prototype and test them before the cosmetic flows.

Step four: build in compliance-aware sprints

The build runs in two-week sprints with a security review embedded in each, not bolted on at the end. Payment endpoints need idempotency keys to prevent double-processing, sensitive data is tokenised before it ever reaches a log, and the card-data environment is network-segmented from the rest of the system.

Step five: the compliance audit and penetration test

A regulated build needs a distinct audit phase, three to six weeks, covering an external penetration test, the SOC 2 or PCI evidence, and the technical attestation the FCA application relies on. Competitors treat this as part of QA; for a regulated product it is its own phase with its own budget.

Step six: launch and post-launch compliance

Launch is not the finish line, because regulated obligations continue. Plan for ongoing transaction monitoring, re-KYC triggers when a customer's risk profile changes, and a suspicious activity report workflow that routes to the National Crime Agency under the Money Laundering Regulations 2017.

The Strong Customer Authentication exemption engine

SCA is where UK builds most often get the architecture wrong, because the rules are not "always prompt for two factors". The UK SCA-RTS in the FCA Handbook sets exemptions that a well-built product applies automatically.

The exemptions include low-value payments under £30, transaction-risk analysis where the provider's fraud rate is low enough, trusted beneficiaries the customer has whitelisted, and recurring transactions of the same amount. Each one is a rule in an exemption engine that decides, per transaction, whether to challenge the user or let the payment through.

Building that engine well is the difference between a friction-heavy app that prompts for authentication on every coffee purchase and a smooth one that challenges only when the risk genuinely warrants it. It is a UK-specific piece of engineering most guides never mention.

AML and KYC: vendor selection is an architecture decision

Choosing your identity and screening providers is not a procurement afterthought; it shapes the onboarding flow, the data residency, and the ongoing-monitoring design. The main UK options each have a different profile.

Onfido, Jumio, Veriff, and Sumsub handle document and biometric verification, while ComplyAdvantage and similar handle sanctions, PEP, and adverse-media screening. The decision turns on UK data residency, false-positive tuning, the cost per verification at your expected volume, and how the provider supports ongoing monitoring rather than one-time onboarding.

Critically, the suspicious-activity workflow routes to the UK National Crime Agency under the Money Laundering Regulations 2017, not the US FinCEN that international guides assume. Designing the KYC stack around UK obligations from the start avoids a costly re-integration when the first compliance review lands.

Safeguarding customer money: the backend rule most guides miss

For a payment or e-money institution, the FCA requires customer funds to be safeguarded, and that requirement shapes the backend ledger design directly. It is a pure UK regulatory-engineering decision that no international guide covers.

Safeguarding means customer money is held in segregated accounts, reconciled daily, and never mixed with the firm's operating funds. The ledger has to track each customer's balance against the safeguarded total, with an audit trail that proves the reconciliation.

Designing this in from the start is straightforward; retrofitting it into a ledger that was not built for it is a rebuild. If your permission involves holding customer money, safeguarding is a first-class architecture requirement, not a compliance footnote.

AI and machine learning in a fintech build

AI has moved from differentiator to expectation in UK fintech, and it adds a distinct workstream to the build. Three uses dominate, and each carries its own cost and governance load.

Fraud detection uses velocity counters, geo-anomaly signals, and a model that scores transactions in real time, which raises the data-pipeline and latency work. Credit scoring for thin-file or credit-invisible applicants, a large global population per the World Bank, uses alternative data and demands explainability so decisions can be justified to a regulator. Robo-advisory and investment features bring MiFID II obligations on suitability and disclosure.

The governance matters as much as the model. A regulated AI feature needs audit logs, explainability, and bias controls, so budget for the model evaluation and documentation, not just the engineering. Most builds should start with an off-the-shelf model and invest in custom training only once the value is proven.

What a fintech build costs and how long it takes in the UK

A UK fintech MVP that performs a regulated activity safely runs £40,000 to £120,000, a mid-market platform £150,000 to £500,000, and an enterprise build beyond £500,000. The regulated-build premium of 10 to 20 percent over an equivalent consumer app reflects the DPIA, PCI scope, SCA flows, audit logging, and penetration testing.

On timeline, a regulated MVP takes four to nine months from kickoff, including the compliance-audit phase, and a full banking-grade product 9 to 18 months. The FCA itself works to a statutory determination period of around three months for a complete payment-institution or e-money application, so factor the authorisation timeline alongside the build.

Project management runs 10 to 15 percent of total cost as a named line, and most qualifying builds reclaim roughly 15 to 20 percent of development spend through the merged R&D scheme, per the gov.uk guidance on Corporation Tax R&D relief. For the wider cost structure across platforms, the App Development Cost guide breaks down each tier.

How to brief and choose a partner

The brief decides the quote quality. Arrive with the regulated activity named, an MVP feature list separated from post-launch, an integration list covering KYC, AML, payments, and Open Banking providers, and a data-residency decision.

Then verify the partner against the regulated reality: at least three live UK fintech products under FCA arrangements, certifications matching your data, a fintech reference architecture, a named UK delivery lead, IP assigned on payment, and an NDA before discovery. The full vendor framework sits in our guide to the top fintech app development companies, and the right partner answers which FCA permission you are pursuing on the first call.

Where this leaves you

Building a fintech app in the UK is a sequencing discipline, not a stack choice. Define the regulated activity, design compliance into the architecture, build in compliance-aware sprints, and treat the audit and post-launch obligations as first-class phases.

The founders who follow that order ship a product that can actually launch and pass FCA scrutiny. The ones who start with the tech stack and treat compliance as a final phase are the ones explaining a six-month overrun in a board paper. If you want a partner who works in that order, our fintech development team builds regulated products end to end for UK founders.

Frequently Asked Questions

How do you develop a fintech app in the UK?

Start by defining the regulated activity and the FCA permission it needs, then design the compliance architecture in discovery before any build. Build in compliance-aware sprints, run a distinct audit and penetration-test phase, launch, and maintain ongoing obligations such as transaction monitoring and re-KYC. The regulated activity, not the tech stack, sets the sequence.

How much does it cost to develop a fintech app in the UK?

A regulated MVP runs £40,000 to £120,000, a mid-market platform £150,000 to £500,000, and an enterprise build beyond £500,000. The regulated-build premium of 10 to 20 percent covers DPIA, PCI scope, SCA, audit logging, and penetration testing. Most qualifying builds reclaim roughly 15 to 20 percent through R&D relief.

How long does it take to build a fintech app?

A regulated MVP takes four to nine months from kickoff, including the compliance-audit phase, and a full banking-grade product 9 to 18 months. The FCA works to a roughly three-month statutory determination period for a complete payment or e-money application, which runs alongside the build.

What compliance does a UK fintech app need?

At minimum FCA authorisation for the regulated activity, PSD2 with Strong Customer Authentication, UK GDPR, and AML and KYC under the Money Laundering Regulations 2017. Card handling adds PCI DSS, investment features add MiFID II, and a payment or e-money permission adds safeguarding of customer money. These are architecture decisions, not a final checklist.

Can a general app developer build a fintech app?

They can write the code, but a fintech build fails on regulatory sequencing, not coding. Without documented FCA-regulated delivery, the right certifications, and a fintech reference architecture, a generalist discovers the compliance load at month four, when retrofitting it costs three to four times more than building it in.