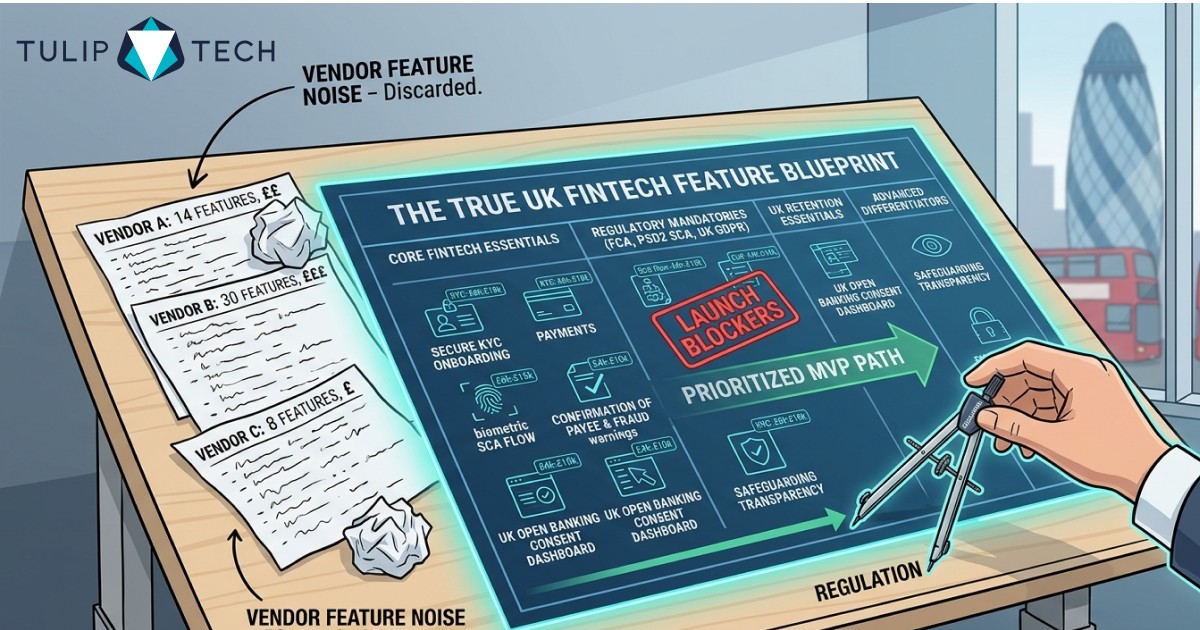

Three vendors quote the same fintech idea and send back three different feature lists at three different prices. One has fourteen features, one has thirty, one has eight, and none of them explains why.

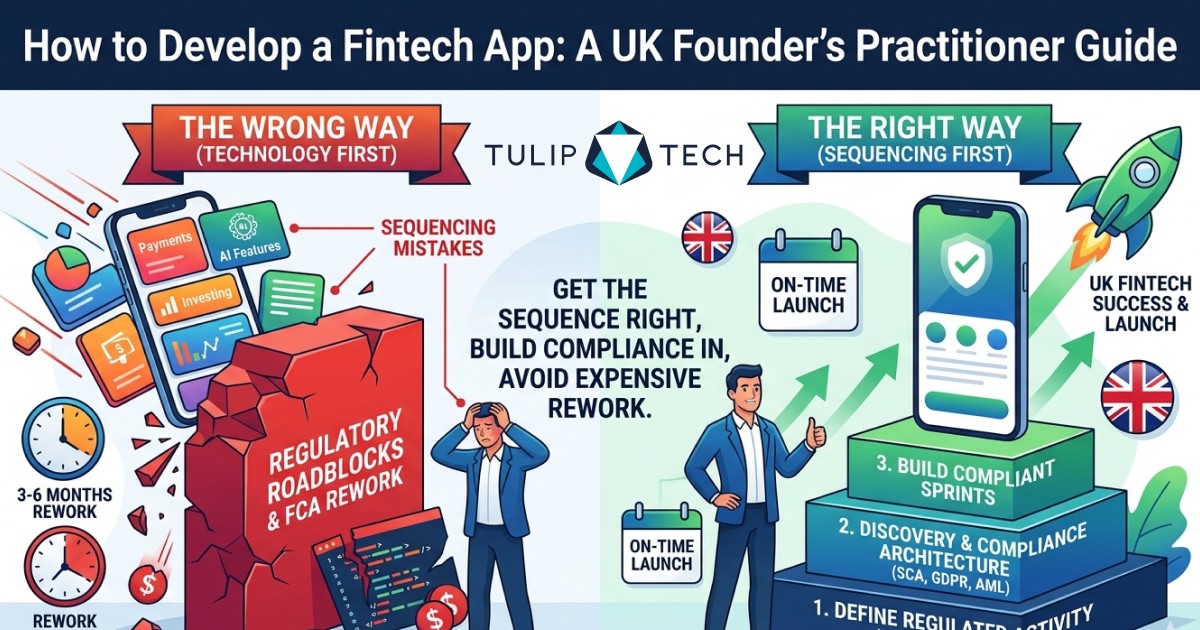

The reason is that "must-have" is not a fixed list. For a UK fintech app it depends on the regulated activity the product performs and what UK GDPR, PSD2, and the FCA require before it can launch at all.

This guide cuts through the vendor noise. It maps the features every UK fintech app actually needs, grouped by purpose, with a UK example and a cost range for each, the regulatory features competitors never mention, and how to prioritise the list for an MVP.

Why "must-have" depends on your regulated activity

A budgeting app that never touches customer money needs a very different feature set from an e-money product that holds it. The regulated activity decides which features are legally mandatory, not just desirable. Choosing the partner who understands that is the subject of our pillar on the top fintech app development companies; this guide maps the features themselves.

The UK context makes this sharper than the global guides assume. EY reports UK fintech adoption at around 71 percent of consumers, the highest in Europe, and over 16 million people now use Open Banking, so UK users arrive expecting bank-grade security, instant payments, and consent control as standard.

That expectation, plus the FCA's rules, turns several features from "nice to have" into launch-blockers. The groups below separate what every fintech app needs from what differentiates one.

The core features every fintech app ships with

These are the features without which the product is not a fintech app. Each carries a UK build-cost range and a UK example.

Secure onboarding and KYC

Identity verification is the front door, and for any regulated product it is mandatory under AML rules. Monzo and Starling set the UK benchmark: photo ID, a liveness selfie, and address checks completed in minutes. Expect £6,000 to £18,000 including the identity-provider integration.

Payments and transfers

Moving money is the core action, whether card payments, bank transfers, or Open Banking initiation. Wise built its reputation on transparent cross-border transfers, and a UK build with a payment-gateway or Open Banking integration runs £8,000 to £20,000 per rail.

Account balances and transaction history

A clear, real-time view of balance and categorised transactions is the screen users open most. Done well, as in Starling's feed, it reduces support load. Expect £5,000 to £15,000 including categorisation logic.

Notifications and alerts

Instant payment notifications are now an expectation, not a feature, and they are also a fraud-control tool. Monzo's instant spend alerts are a textbook example. Budget £2,000 to £5,000 including segmentation.

The security and compliance features that are non-negotiable

For a UK fintech these are not optional, because the product cannot legally operate without them.

Strong Customer Authentication

The FCA's onshored SCA rules require multi-factor authentication on payments, in force since 2022. The skill is delivering it without killing conversion, using step-up authentication and the permitted exemptions.

Biometric SCA, which Visa research suggests 46 percent of consumers trust more than passwords, is the standard UK approach. Expect £6,000 to £15,000 for a proper SCA flow.

Confirmation of Payee and fraud warnings

The UK's mandatory APP-fraud reimbursement rules make Confirmation of Payee and in-flow fraud warnings a UK-specific must-have no global guide mentions. The feature checks that the payee name matches the account before a transfer completes, cutting authorised-push-payment fraud. Budget £4,000 to £10,000.

Encryption, fraud detection, and audit logging

Data must be encrypted in transit and at rest, transactions scored for fraud in real time, and every action written to an immutable audit log for regulatory review. These are architecture, not screens, and together add £10,000 to £30,000 depending on the fraud-model depth.

The UX features that decide retention

Compliance gets you to launch; UX decides whether users stay. These features separate a fintech app people keep from one they delete.

Fast onboarding and a clear dashboard

Every extra onboarding step costs conversion, so the best UK apps front-load value and defer non-essential verification where the rules allow. A clean dashboard with the next action obvious is the retention workhorse. Expect £8,000 to £20,000 for a polished onboarding and dashboard.

In-app support and human escalation

Financial questions are anxious questions, so in-app chat with a clear path to a human matters more than in most apps. Research cited by getstream links live chat to materially better outcomes. Budget £5,000 to £15,000 for chat with escalation workflows.

Personalisation and spending insights

Categorised spending, budgets, and tailored insights turn a utility into a habit. Starling and Monzo both lean on this. Expect £6,000 to £18,000, more if AI-driven.

The advanced features that differentiate

These are not required to launch, but they are where a fintech product wins a segment. Add them once the core and compliance features are solid.

Open Banking aggregation

Pulling in accounts from other banks via Open Banking turns a single-product app into a money hub. With 16 million UK users, this is increasingly expected. Expect £10,000 to £25,000 including the aggregator integration.

Robo-advisory and AI insights

Automated investment guidance or an AI financial assistant differentiates a wealth or budgeting product, but robo-advisory brings MiFID II suitability obligations. Budget £15,000 to £50,000 depending on the model and governance.

Multi-currency and cross-border payments

For any product serving international users, multi-currency accounts and transparent FX are a strong differentiator, as Wise and Revolut show. Expect £12,000 to £35,000 per the scope of currencies and rails.

BNPL, crypto, and gamification

Buy-now-pay-later, crypto rails, and gamified saving each open a segment and each carries its own regulatory and engineering load. Cost varies widely, from £8,000 for a savings-streak feature to £40,000+ for compliant crypto handling.

The UK regulatory features competitors leave out

Every global feature guide stops at "add MFA". A UK fintech needs several features that exist purely because of UK rules, and missing them blocks launch or invites enforcement.

Open Banking consent management

For the 16 million UK Open Banking users, the consent journey is a feature in its own right: granting access, a consent dashboard, and the mandatory 90-day re-authentication. A clear consent experience is both a legal requirement and a trust signal. Budget £6,000 to £15,000.

Safeguarding transparency

A UK e-money or payment institution must safeguard customer funds, and surfacing that status in-app, along with clarity on FSCS coverage where it applies, builds trust no global competitor addresses. This is a UX layer over a backend obligation, at £3,000 to £8,000.

Accessibility and the Consumer Duty

Under the FCA Consumer Duty and vulnerable-customer guidance, accessibility is a regulatory expectation, not a nicety. WCAG 2.2 AA, screen-reader support, plain-English balances, and carer or third-party access serve financial inclusion and compliance at once. Expect 10 to 15 percent added across the build.

What the feature set costs and how to read a quote

Adding the groups above, a UK fintech MVP with core, security, and compliance features lands at £40,000 to £120,000, with advanced features pushing a full build to £150,000 and beyond. Annual maintenance runs 15 to 25 percent, and most qualifying builds reclaim roughly 15 to 20 percent through R&D relief.

This is why three vendors quote three numbers: they are each assuming a different feature set behind the same one-line brief. A quote that lists features with a cost against each, rather than a single headline number, is the one you can actually compare, and it is the sign of a partner who has built regulated products before.

How to prioritise features for an MVP

You cannot build everything first, and for a regulated product the cut list is not obvious. The rule is simple: keep every feature the regulated activity legally requires, and defer everything that only adds breadth.

Keep KYC onboarding, the core payment or account action, SCA, fraud controls, and audit logging, because without them the product cannot legally operate. Defer the second account type, advanced analytics, gamification, and most advanced differentiators to version 1.1. Prioritise the one feature that proves your specific value, and build everything else around making that feature usable and compliant.

That sequence ships a smaller, launchable product faster, and it is the discipline that separates a fintech MVP that reaches paying users from one that runs out of runway mid-build.

Where this leaves you

Must-have features for a UK fintech app are decided by the regulated activity first and the user experience second. The core, security, and compliance features are launch-blockers; the advanced and UK-regulatory features are where the product earns trust and differentiates.

Map your features to the activity your product performs, cost each one, and prioritise the compliance-critical set for the MVP. If you want a feature list and cost mapped to your specific regulated activity, our fintech development team scopes regulated builds for UK founders end to end.

Frequently Asked Questions

What features does a fintech app need to launch in the UK?

At minimum, secure KYC onboarding, the core payment or account feature, Strong Customer Authentication, real-time fraud detection, audit logging, and balance and transaction views. These are legally required for a regulated product. UX features such as a clean dashboard and in-app support decide retention but are not launch-blockers.

How much do fintech app features cost in the UK?

Individually, KYC onboarding runs £6,000 to £18,000, a payment rail £8,000 to £20,000, an SCA flow £6,000 to £15,000, and Open Banking aggregation £10,000 to £25,000. A full UK fintech MVP with core and compliance features lands at £40,000 to £120,000, with advanced features pushing a build beyond £150,000.

What UK-specific features do fintech apps need?

Beyond global security features, a UK fintech needs FCA-compliant Strong Customer Authentication, Confirmation of Payee with fraud warnings under the APP-fraud rules, Open Banking consent management with 90-day re-authentication, safeguarding transparency for e-money firms, and accessibility under the FCA Consumer Duty. Global feature guides omit all of these.

Which fintech features should an MVP include?

Keep every feature the regulated activity legally requires: KYC, the core payment or account action, SCA, fraud controls, and audit logging. Defer breadth features such as a second account type, advanced analytics, and gamification to version 1.1. Prioritise the single feature that proves your value, then make it usable and compliant.

What is Confirmation of Payee and why does a UK fintech app need it?

Confirmation of Payee checks that a payee's name matches their account before a transfer completes, reducing authorised-push-payment fraud. The UK's mandatory APP-fraud reimbursement rules make it a practical must-have for any UK payment app, and no global feature guide covers it.