It is a Tuesday morning in March. A UK fintech founder is on a call with their development partner, and the product that should have launched six weeks ago has not.

The Strong Customer Authentication architecture does not match what PSD2 actually requires. The original quote was £180,000; the current burn is £290,000. The Financial Conduct Authority application has not started, because the technical attestation needs a rewrite.

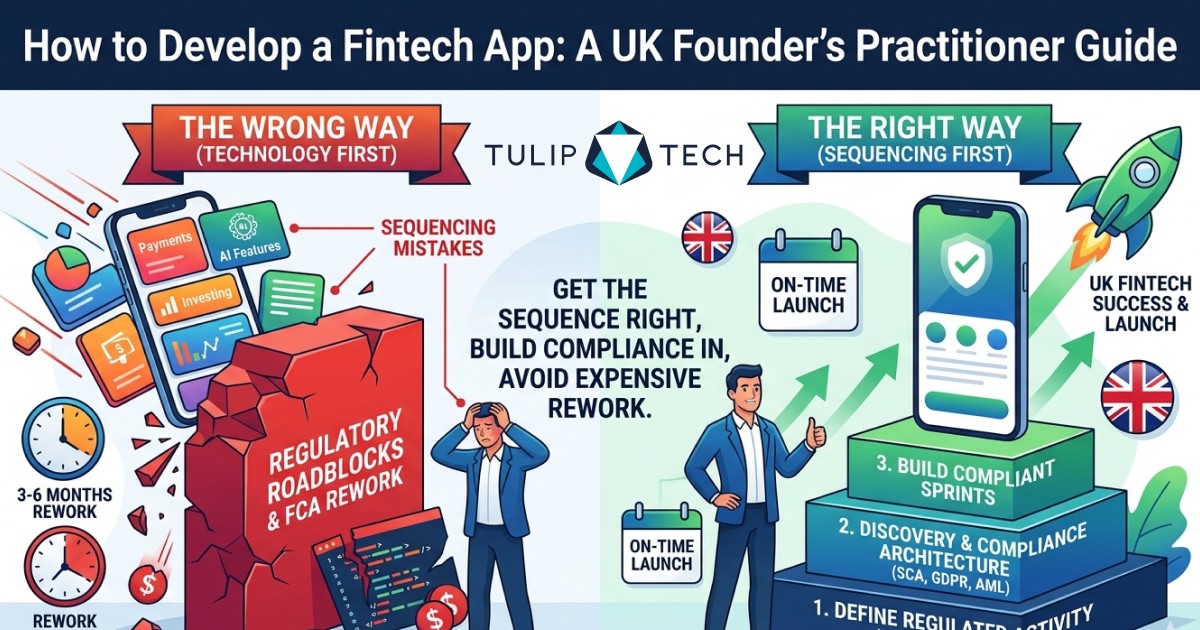

The team is competent and the code is clean. None of that helps when the build never accounted for the regulatory environment it was always going to launch into. This is the most common reason a UK fintech build fails, and it is a vendor-selection failure, not a coding one.

The companies below all build fintech apps for UK clients, but the part that matters most is the framework that decides which one fits your product, your stage, and your regulatory position.

Why vendor selection is the single biggest risk in a UK fintech build

The UK fintech opportunity is real. Mordor Intelligence values the UK fintech market at around 18.6 billion US dollars in 2025, rising toward 43.9 billion by 2031, and the FCA reports that 75 percent of UK adults now use fintech services. UK Open Banking passed 16 million active users in 2025, with payments through the system growing more than 50 percent year on year.

So is the regulatory floor. Any product handling UK customer money or payment data sits inside at least three frameworks: FCA authorisation, PSD2 including Strong Customer Authentication, and UK GDPR, with PCI DSS added for card handling and AML and KYC on top.

A partner who has shipped consumer apps but not regulated financial products will not see those frameworks until they hit them. Nine times out of ten, when a build runs over budget, the code is fine and the compliance architecture has to be retrofitted, which costs three to four times more than building it in from the start.

How we selected these companies

Transparency matters on a list like this, so here is the method. We started from a wider set of UK and UK-serving fintech development firms and scored each against six weighted criteria.

We weighted documented FCA-regulated delivery history, security certifications matching the data handled, a fintech reference architecture, UK regulatory proximity, transparent IP and pricing terms, and a credible post-launch model. We did not weight raw headcount, awards, or self-reported client counts, because none of those predicts whether a regulated build ships.

The result is a shortlist ordered by fintech specialisation and UK regulatory proximity, not by size. Before signing with any firm here, check its current rating on Clutch or GoodFirms and ask for two reference clients with live FCA-regulated products, because a list is a starting point and your own due diligence is the finish.

The three root causes of failed UK fintech builds

Three failure modes account for most UK fintech projects that come in over budget or never ship. Recognising them in the evaluation is the difference between a quote that holds and one that does not.

A generic agency picked on price

UK rates run £500 to £625 per day for a senior developer, regional agencies £350 to £550, and offshore teams £20 to £40 per hour. The headline gap is real, but a fintech-naive partner needs more discovery, more rework on compliance gaps, and more architecture revisions when the regulatory consequences land. The cheaper rate is rarely the cheaper project.

Compliance treated as a post-build audit

FCA, PSD2, and GDPR decisions live in the data model, the authentication flow, the API surface, and the deployment region. None of those are post-build choices. A partner who proposes to handle compliance "during testing" is signalling that they do not understand the work, because by testing the architecture is already set and expensive to undo.

Discovery skipped to save money

A fixed-price quote accepted before the spec is defined fills the gaps with the partner's cheapest assumption, rarely your most-compliant one, and the renegotiation arrives at month three. Discovery for a UK fintech build runs £8,000 to £15,000 over three to five weeks, and skipping it saves nothing, because building the wrong thing adds 30 to 50 percent to the budget.

What good preparation looks like before you choose a partner

A well-prepared founder arrives at vendor selection with five things written down, each of which changes the quality of every quote that comes back.

First, which regulated activity the product performs: payment institution, electronic money institution, credit broker, or exempt support tool, because that decides the FCA pathway. Second, a feature list split into the MVP that proves the regulated activity works and the post-launch features that should not block the submission.

Third, a list of every integration the app needs: KYC and AML providers, payment processors, core banking partners, and Open Banking aggregators. Fourth, a confirmed budget range and a walk-away maximum, which produces honest proposals. Fifth, a decision on where the data will live, because UK GDPR and FCA expectations push toward UK or EEA hosting and retroactive changes cost real money.

The regulatory floor every fintech build must clear

Competitors mention "FCA compliance" as a checkbox. The reality is four named regimes, and your partner must build for each one.

FCA authorisation: the permission your product needs, from payment-institution to e-money to AISP or PISP status, which shapes the entire build.

PSD2 and Strong Customer Authentication: the multi-factor flows and Open Banking obligations that sit in the authentication architecture.

UK GDPR: with a maximum fine of £17.5 million or 4 percent of global turnover, whichever is higher, per the ICO, which makes data architecture a board-level risk.

PCI DSS and AML/KYC: card-data scope under PCI DSS v4.0, plus anti-money-laundering and know-your-customer obligations under the Money Laundering Regulations 2017.

A partner who can name how each regime touches the build, before the discovery call, is demonstrating the experience that prevents the month-four retrofit.

The FCA authorisation interplay most founders miss

Here is the single biggest unaddressed risk in vendor selection: your development partner does not hold your FCA authorisation. You do, or your principal firm does, and a build can be technically perfect yet stall at the FCA gateway if it was not built for the specific permission you are applying for.

A payment institution, an e-money institution, and an account or payment information service provider under PSD2 each carry different technical obligations. Briefing a vendor for a generic "compliant app" rather than your target permission is how a build and an authorisation application end up describing two different products.

Brief the partner against your target permission from day one, and require the discovery output to map the build to that permission. The vendor that asks which authorisation you are pursuing on the first call is the one that has done this before.

Open Banking as a build decision, not a buzzword

If your product touches account or payment data, you face a decision competitors never explain: become a regulated third-party provider yourself, an AISP or PISP, or integrate a regulated provider's API.

Becoming a TPP gives you control and removes a per-transaction fee, at the cost of your own FCA authorisation, ongoing compliance, and a longer build. Integrating a licensed aggregator's API is faster and shifts the regulatory burden, at the cost of a dependency and usage fees. Each path changes the build cost, the timeline, and how much FCA work you carry.

The right choice depends on whether Open Banking is your core product or a feature of it. A partner should be able to model both paths for you, because the decision shapes the architecture before a line of code is written.

How to evaluate the top fintech app development companies

Eight criteria separate the firms that deliver from the ones that quote competitively and disappoint at month four. Treat each as a yes or no.

Documented FCA-regulated delivery history: at least three live UK fintech products under FCA authorisation or appointed-representative arrangements, with named references.

Compliance architecture in discovery, not testing: the discovery output maps FCA pathway, PSD2 SCA, GDPR data flows, and KYC/AML before the build quote is finalised.

Security certifications matching the risk: ISO 27001, Cyber Essentials Plus, and SOC 2 Type II, plus PCI DSS attestation for any card-handling build.

A specialised reference architecture: a banking core, an Open Banking aggregator, an identity-verification provider, and a fraud-monitoring layer, rather than a generic mobile case study.

UK time zone and regulatory proximity: a UK HQ, registered office, or senior delivery lead in-country, because FCA, PSD2, and ICO exchanges happen in UK hours.

Project management as a named cost line: at 10 to 15 percent of total cost, never hidden in the developer rate.

Transparent pricing and engagement model: fixed price for defined scope, time and materials for unclear scope, retainer for post-launch, matched to your stage rather than their margin.

IP ownership and exit clauses: full assignment of code, design, and documentation at handover, with an exit clause that lets you move the work without penalty.

The top fintech app development companies in the UK for 2026

The firms below all deliver fintech app development for UK clients, ordered by fintech specialisation and UK regulatory proximity rather than size. Each entry covers location, fintech focus, regulated experience, and the project it suits best. Verify each firm's current Clutch or GoodFirms rating before shortlisting.

1. TulipTech

Headquarters Leicester, UK, with delivery offices in Dhaka, Ahmedabad, and Sharjah, building regulated products for 14+ years across fintech, healthcare, retail, and enterprise SaaS. ISO 27001 and Cyber Essentials certified, a Microsoft Technology Partner and Odoo Ready Partner, with IP assigned on payment and an NDA before discovery.

Best for UK fintech founders and SMEs who want a UK delivery lead, regulated-build experience, and transparent pricing from MVP to enterprise.

2. Foundry 5

A London fintech agency with an AI-first approach and a documented FCA-regulated delivery record, embedding compliance from week one and shipping MVPs in as little as four weeks. The team is UK-concentrated, keeping regulatory communication in one time zone.

Best for UK founders building a regulated fintech MVP under time pressure where FCA scoping cannot wait for a separate phase.

3. Endava

A London-headquartered enterprise technology firm founded in 2000 with more than 12,000 staff, covering payments infrastructure, card processing, digital banking, and capital markets for UK retail and investment banks.

Best for enterprise fintech transformation and payments modernisation where the build integrates with existing core banking systems.

4. Studio Graphene

A London product studio handling full-cycle cross-platform and web builds, weighted toward fintech, healthcare, and EdTech, focused on investor-ready MVPs. Cross-platform stacks keep upfront cost below dual-native builds.

Best for pre-Series A fintech founders who need one partner from product strategy through a shipped MVP and value design quality.

5. SPD Technology

A UK-aligned fintech firm with a long track record of regulated financial products across digital banking, lending, and wealth, with a reference architecture covering Open Banking, KYC and AML, and PCI DSS-aligned payments.

Best for established fintechs scaling beyond MVP that need a partner who has shipped FCA-regulated products before.

6. Apadmi

A Manchester-based mobile specialist with enterprise and financial-services clients, strong on native and cross-platform delivery with UK-based teams and security practices suited to regulated work.

Best for UK businesses that want a substantial UK-based mobile partner with enterprise delivery discipline.

7. Waracle

A UK digital product company with offices across Scotland and London, with a deep financial-services and healthcare portfolio and experience of regulated, security-sensitive builds.

Best for UK fintech and health products that need a UK-based partner comfortable with compliance-heavy delivery.

8. DataArt

A global technology consultancy with around 5,000 engineers and a strong financial-services practice in core banking modernisation, capital markets, and trading platforms, with an established UK presence.

Best for large-scale fintech transformation inside an existing institution, where modernisation runs alongside live production systems.

9. Netguru

A Polish fintech specialist with around 700 engineers, roughly 40 percent of its portfolio in fintech, strong on digital banking, BaaS APIs, and Open Banking, at nearshore rates with a one-hour time difference.

Best for UK fintechs building digital banking or Open Banking products who want specialisation at nearshore rates.

10. Innowise

A global engineering firm with 3,500+ engineers and a decade-plus UK fintech practice, with a reference architecture covering neobank cores, cloud banking, and EU regulatory frameworks, able to staff parallel workstreams.

Best for scale-up and enterprise fintech builds that need multiple workstreams run in parallel.

11. DashDevs

An Estonia-based fintech specialist publishing a white-label neobank core with hundreds of API endpoints and full source-code handover, compressing platform engineering into a configured deployment.

Best for founders launching a neobank, wallet, or payments product quickly on an opinionated platform.

12. 10Pearls

A US and UK-presence product firm with over 1,000 engineers and a fintech practice in AI-driven lending, credit, and digital wealth, strong at integrating AI tooling into regulated workflows.

Best for fintech businesses whose differentiator is intelligence on top of standard fintech rails, such as credit decisioning or fraud detection.

The fintech trends shaping your build in 2026

The build you commission should account for where UK fintech is heading, because the partner's reference architecture either anticipates these or does not.

AI fraud detection and credit decisioning are moving from differentiator to expectation, which raises the data and model-governance work in a build. Embedded finance and Banking-as-a-Service let non-banks offer financial products through APIs, changing whether you build a full stack or integrate one. Real-time payments and the continued growth of Open Banking are reshaping what customers expect a fintech app to do on day one.

A partner whose reference architecture already includes these is quoting for the product you will need in two years, not the one that was current two years ago.

The funding climate as a build-budget input

UK fintech funding tightened in 2025. Innovate Finance reports UK fintech attracted 3.6 billion US dollars across 534 deals, keeping the UK second globally, while KPMG, on a different methodology, recorded a five-year low. Either way, founders are building leaner than they were.

That should shape scoping, not just morale. A tighter climate favours an MVP-first build that proves the regulated activity and the unit economics before the full feature set, with the regulated-build premium of 10 to 20 percent budgeted from the start rather than discovered later. Runway-aware phasing, where each stage is funded by the evidence the last one produced, is the sensible response to a market that rewards proof over promise.

The pre-commit checklist before you sign any contract

The shortlist call is the last point at which you can verify what a partner delivers. Any firm that struggles with three or more of these is signalling a delivery risk.

Can you name three live UK fintech products you shipped under FCA authorisation, and can we speak to one client? What is your discovery deliverable, and does it cover FCA pathway, PSD2 SCA, GDPR data flows, and KYC/AML? Which security certifications do you hold, and which apply to our data?

Do you bring a fintech reference architecture, and which banking core, identity, and payments providers do you integrate? Where will the build team physically sit, and who is the named UK delivery lead with regulatory accountability?

Is project management a named line at 10 to 15 percent? Which engagement model are you proposing, and why does it fit our stage? Does the contract assign full IP at handover with a clean exit clause?

Data residency and the UK adequacy question

One question every fintech buyer should ask, and no competitor list covers, is where your data physically lives. UK GDPR and FCA expectations favour UK or EEA hosting for consumer financial data, and the UK-EU data adequacy arrangement governs cross-border flows.

For any partner with offshore delivery, this is a transparency test, not a disqualifier. A credible partner answers it with a clear data-processing agreement, a named hosting region, and a data-flow design that keeps personal financial data within an adequate jurisdiction. The honest answer to "where does our data live and who can access it" tells you as much about a partner as any certification.

What to read next and how to choose

Vendor selection is one of three decisions a UK fintech founder makes before commissioning a build. If the partner fits but the brief needs work, our how to develop a fintech app guide goes deeper on discovery, design, and compliance.

If the brief is clear but the feature scope is open, the must-have features for a fintech app guide maps the regulated UK components in detail. For the underlying cost structure across platforms, the App Development Cost in the UK guide breaks down each tier.

The firm you pick should match three things at once: the regulated activity your product performs, the stage you are at, and the engagement model that fits how clearly your scope is defined. The cheapest day rate is rarely the cheapest project, and the compliance retrofit at month four is the line that separates the builds that ship from the ones explained in a board paper six months late. Our team builds regulated fintech products end to end and is glad to be one of the partners you compare.

Frequently Asked Questions

What is the best fintech app development company in the UK?

There is no single best fintech app development company in the UK. The right partner depends on the regulated activity, the stage of the build, and the engagement model. For an MVP under time pressure, a UK boutique with FCA-aligned delivery experience usually fits; for enterprise transformation, an established consultancy with banking-core integration history is more appropriate.

How much do top fintech app development companies charge in the UK?

UK fintech companies typically charge £500 to £625 per day for senior engineers, with London-senior agencies at £600 to £900 and nearshore agencies at £28 to £60 per hour. Offshore agencies run £20 to £40 per hour. Total project cost depends more on scope clarity and regulatory complexity than on the day rate alone.

How do I shortlist fintech app developers for an MVP?

Shortlist on three signals: documented FCA-regulated delivery of at least three live products, security certifications matching the data the product handles, and a discovery deliverable that explicitly covers FCA pathway, PSD2 SCA, GDPR, and KYC/AML. Anything below that floor is a delivery risk for a regulated build.

Should I use a UK or offshore fintech app development agency?

UK agencies suit unclear-scope projects with active regulatory dependencies, because the time-zone overlap shortens every FCA, ICO, and partner exchange. Nearshore suits defined-scope projects where cost matters more than proximity, and offshore suits fully specified work with strong UK-side product management. The cheapest agency is rarely the cheapest project for a regulated fintech.

What certifications should a fintech app development company hold?

ISO 27001 is the minimum for any partner handling personal financial data, Cyber Essentials Plus is the UK baseline, and SOC 2 Type II is preferred for partners delivering to financial institutions. PCI DSS attestation is required if the partner will touch card data. A partner without ISO 27001 should not be on a fintech shortlist.